If there is one phrase that has caused more confusion and more financial heartburn among investors in recent years, it is:

“Assured Returns.”

It looks comforting.

It sounds safe.

It feels risk-free.

But the reality?

It’s often the most misunderstood promise in the entire investment world.

As your wealth advisors, our goal is to help you understand what’s behind the curtain not to scare you, but to empower you. So, the next time someone offers you “guaranteed 12–18% returns,” you’ll know exactly what questions to ask… and what traps to avoid.

The Psychology Behind ‘Assured’

We all love certainty.

And in a world where markets move daily, the idea of something “fixed” or “guaranteed” feels like financial comfort food.

That’s why the word assured is so powerful it instantly reduces fear.

But here’s the truth most investors don’t hear:

In finance, the word ‘assured’ almost never means what you think it means.

It is usually a marketing phrase, not a legal guarantee.

🔍 The Fine Print No One Reads — But Should

Here’s a simple rule:

The bigger the assured return, the smaller the actual guarantee.

Let’s understand what typically hides inside the fine print.

1️⃣ It’s Not Assured — It’s “Projected”

Many investment brochures show 8%, 12%, or even 16% “assured returns” …

but the fine print usually says:

- illustrative return

- based on past performance

- subject to fund performance

Meaning?

They’re showing you a best-case scenario, not a promise.

2️⃣ The Guarantee Is Conditional Very Conditional

You only get the “assurance” if:

✔ you stay invested for 10–20 years

✔ you pay every premium on time

✔ you never withdraw early

✔ the company continues declaring bonuses

✔ there are no administrative or hidden charges

Miss even one?

The promised return usually disappears.

3️⃣ Fees Eat into Your ‘Assured’ Return

From policy allocation charges to fund management fees and surrender charges

a lot of “assured return” products hide costs that slowly erode returns.

It’s like being promised a full plate of biryani…

but the waiter keeps removing spoons from it every few minutes.

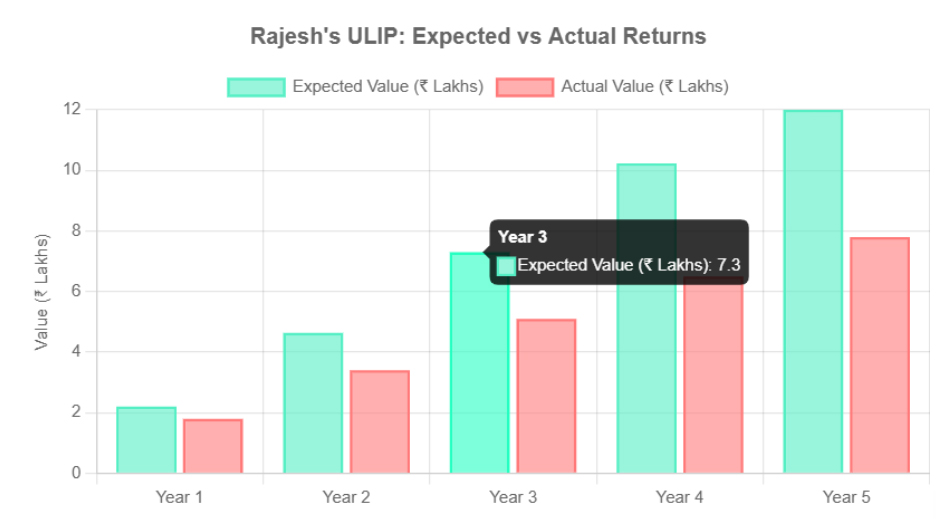

📌 Example 1: The 10% ULIP Surprise

Rajesh, 44, invested ₹2 lakhs per year in a ULIP with “10% assured return.”

But after 5 years, when he checked his value, it was ₹7.8 lakhs, not the ₹12 lakhs he expected.

Why?

The 10% was not guaranteed annually it was only a maturity benefit after 15 years based on future bonus declarations.

📌 Example 2: The ‘Safe’ Corporate FD

Priya, a retired teacher, invested in an FD offering 11% assured returns.

The company defaulted.

Unlike bank FDs, corporate FDs are not insured.

Her “assurance” turned into litigation.

📌 Example 3: Property with Assured Rentals

Amit, 38, put ₹25 lakhs into a real estate project promising “10% assured rental for 3 years.”

The developer paid for a year… then vanished.

There was no legally enforceable contract.

The Hidden Truth: Why High Return = Higher Risk

Here’s what most investors don’t realize:

Those offering “12% guaranteed” returns are usually companies with lower credit ratings.

That means the risk of delay or default is significantly higher.

Below is a simple credit rating guide:

Credit Rating | What It Means |

|---|---|

AAA | Very Safe |

AA | Safe |

A | Moderate Safety |

BBB | Borderline Risk |

BB/B/C/D | High to Default Risk |

Most “11–12% assured return” schemes fall into the BBB or lower category — exactly where risk starts rising sharply.

What Risks Do These Offers Carry?

- The company may delay interest payments

- The company may default entirely

- You may enter a long legal recovery process

- Secondary market liquidity may be poor

- In a crisis, investors usually get paid last

Remember the major financial failures of recent years:

- IL&FS

- DHFL

- Yes Bank AT1 Bonds

In all these cases, investors who believed in “high but safe return” offers suffered significant losses.

A Smarter Way to Seek Higher Income

High-yield investments are not inherently bad.

They simply require professional risk management, which retail investors usually do not have the tools to perform.

A more suitable approach is:

✔ Credit Risk Mutual Funds

These funds offer:

- Expert selection of bonds

- Diversification across multiple issuers

- Better liquidity

- SEBI-regulated transparency

- Lower impact if one company defaults

Consider this scenario:

If you invest ₹5 lakh in one high-risk bond →

and it defaults → your capital is severely affected.

If you invest ₹5 lakh in a credit risk mutual fund →

even if one company fails, the remaining portfolio absorbs the damage, lowering the impact.

This is why professionals prefer diversified debt strategies instead of isolated high-yield bonds.

🟥 Before Believing Any “Guaranteed Return,” Ask These Questions

- Who is guaranteeing it?

A government entity or a private company struggling for capital? - Is the guarantee legally written in the official contract?

Not just in a brochure or verbal promise. - What is the credit rating of the issuer?

- What happens if I need to exit early?

Many such products have harsh penalties or zero liquidity. - If this return was truly risk-free, why are banks and institutions not investing in it?

🟩 Final Thought: Safety Should Always Come Before Returns

At Opulence Wealth, we believe that:

- Wealth creation is a marathon, not a sprint.

- Capital protection comes before high returns.

- Clarity matters more than marketing promises.

So the next time you see:

“Assured 12% return!”

Pause and ask:

Is this a financial opportunity — or a financial trap?

Your hard-earned money deserves honest advice, transparent products, and risk-aware planning.

Whenever you’re in doubt, share the product with us — we will gladly decode the fine print and guide you toward safer, smarter choices.